Estate planning is a critical financial process that extends far beyond the realm of the wealthy, which is why estate planning for accountants is so important. As trusted financial advisors, accountants play a pivotal role in guiding clients through the complexities of estate planning, ensuring their assets are protected and distributed according to their wishes. This comprehensive guide explores how accounting professionals can leverage their expertise to provide invaluable assistance in estate planning, ultimately helping clients secure their financial legacy.

The importance of estate planning cannot be overstated, regardless of an individual’s financial status. Many people mistakenly believe that estate planning is only necessary for those with substantial wealth. However, this misconception often leads to overlooking the assets one actually possesses. In reality, nearly everyone has an estate—whether it consists of a home, savings accounts, personal belongings, or investments—and therefore requires a well-thought-out estate plan.

As an accountant, your role in estate planning is multifaceted and crucial. Your intimate knowledge of your clients’ financial situations, combined with your expertise in tax laws and financial planning, positions you uniquely to offer comprehensive estate planning guidance. By expanding your services to include estate planning assistance, you not only provide added value to your clients but also strengthen your professional relationships and potentially increase your practice’s revenue streams.

In this guide, we will delve into the various aspects of estate planning where accountants can make significant contributions. From asset valuation and tax optimization to succession planning and trust administration, we’ll explore how you can leverage your skills to help clients navigate the complex landscape of estate planning. Let’s embark on this journey to understand how accountants can become indispensable partners in their clients’ estate planning endeavors.

Understanding the Accountant’s Role in Estate Planning

As an accountant, your involvement in estate planning goes beyond mere number-crunching. Your role is that of a strategic advisor, leveraging your financial acumen to help clients make informed decisions about their estate. Here’s a closer look at the multifaceted role you can play:

Financial Gatekeeper

Your position as a financial gatekeeper is invaluable in the estate planning process. You have a comprehensive understanding of your clients’ financial situations, including their assets, liabilities, and cash flow. This knowledge allows you to identify potential issues and opportunities that may impact their estate plan.

For instance, you might notice that a client’s investment portfolio is heavily weighted towards a single stock, which could pose risks to their estate’s value. By bringing this to their attention, you can help them diversify their holdings and protect their estate’s long-term value.

Tax Strategy Expert

One of the most crucial aspects of estate planning is minimizing tax liabilities. As an accountant, you’re well-versed in tax laws and regulations, making you an ideal advisor for tax-efficient estate planning strategies. You can guide clients on how to structure their assets and make strategic decisions to reduce estate taxes, gift taxes, and income taxes for beneficiaries.

For example, you might recommend strategies such as setting up irrevocable life insurance trusts or making annual gifts to family members to reduce the taxable estate. Your expertise in this area can result in significant tax savings for your clients and their heirs.

Asset Valuation Specialist

Accurate asset valuation is critical in estate planning. As an accountant, you have the skills to assess the value of various assets, from real estate and businesses to investments and personal property. This expertise is crucial when it comes to equitable distribution of assets among beneficiaries and for tax reporting purposes.

Your ability to provide precise valuations can help prevent disputes among heirs and ensure that the estate plan accurately reflects the client’s wishes. Moreover, it can help in strategizing how to distribute assets in the most tax-efficient manner.

Succession Planning Advisor

For clients who own businesses, succession planning is an integral part of estate planning. Your understanding of business finances and operations makes you an ideal advisor in this area. You can help clients develop strategies for transferring ownership, whether it’s to family members or through a sale to employees or outside parties.

Your role might involve assessing the financial implications of different succession scenarios, advising on tax-efficient transfer methods, and helping to structure buy-sell agreements. This guidance is crucial in ensuring the smooth transition of a business and preserving its value for the next generation.

Compliance Monitor

Estate planning involves adhering to various legal and regulatory requirements. As an accountant, you can help ensure that all financial aspects of the estate plan comply with current laws and regulations. This includes staying up-to-date with changes in tax laws that might affect estate plans and advising clients on necessary updates.

Your vigilance in this area can prevent costly mistakes and legal issues down the line, providing peace of mind to your clients and their families.

By embracing these diverse roles, you position yourself as an indispensable partner in your clients’ estate planning for accountants journey. Your comprehensive approach not only adds value to your services but also helps clients achieve their long-term financial and legacy goals.

Initiating the Estate Planning Conversation

Broaching the topic of estate planning with clients can be challenging, as it involves discussing sensitive subjects like mortality and wealth distribution. However, as their trusted financial advisor, you are in a unique position to initiate this crucial conversation. Here’s how you can approach this delicate subject effectively:

Emphasizing the Importance of Early Planning Is Essential To Estate Planning For Accountants

One of the key messages to convey is the significance of early estate planning. Many clients may believe they are too young or don’t have enough assets to warrant an estate plan. Counter this misconception by explaining that estate planning is not just about wealth distribution but also about ensuring their wishes are respected in various scenarios, including incapacitation.

Highlight that early planning allows for more flexibility and can potentially save significant amounts in taxes and legal fees. Use examples to illustrate how procrastination in estate planning can lead to unintended consequences, such as assets being distributed against their wishes or excessive tax burdens on their heirs.

Integrating Estate Planning into Regular Financial Reviews

A natural way to introduce estate planning is by incorporating it into your regular financial review meetings with clients. As you discuss their overall financial health, investments, and long-term goals, seamlessly transition into how these aspects tie into estate planning.

For instance, when reviewing a client’s investment portfolio, you might say, “These investments have performed well. Have you considered how you’d like these assets to be managed or distributed in the future as part of your estate plan?” This approach contextualizes estate planning within their broader financial picture.

Addressing Common Concerns and Misconceptions

Be prepared to address common concerns and misconceptions about estate planning. Many clients may worry about the complexity or cost of creating an estate plan. Assure them that the process can be tailored to their specific needs and that the long-term benefits often outweigh the initial investment.

Some clients might be hesitant due to the emotional nature of the topic. Acknowledge these feelings and emphasize that estate planning is an act of care for their loved ones, providing clarity and reducing potential conflicts in the future.

Utilizing Life Events as Conversation Starters

Major life events often serve as natural triggers for estate planning discussions. Events such as marriages, births, divorces, or significant changes in financial status can all necessitate updates to an estate plan. When clients inform you of such events, use these as opportunities to discuss how their estate plan might need to be adjusted.

For example, if a client mentions the birth of a grandchild, you might say, “Congratulations! Have you thought about how you might want to include your new grandchild in your estate plan?”

Providing Educational Resources

Offer clients educational materials about estate planning. This could include brochures, articles, or links to reputable online resources. By providing information upfront, you allow clients to familiarize themselves with the basics of estate planning at their own pace, which can make subsequent discussions more productive.

Consider hosting seminars or webinars on estate planning basics. This not only educates your clients but also positions you as a knowledgeable resource in this area.

Collaborating with Legal Professionals

Emphasize that estate planning is a collaborative effort involving various professionals, including attorneys. Let clients know that you can work in tandem with legal experts to ensure all aspects of their estate plan are comprehensively addressed.

Offer to facilitate introductions to estate planning attorneys if clients don’t already have one. This collaborative approach can make the process less daunting for clients and ensure that both financial and legal aspects are properly aligned.

By approaching the estate planning conversation with sensitivity, knowledge, and a focus on the client’s overall financial well-being, you can effectively guide them towards taking this crucial step in securing their financial legacy.

Conducting a Comprehensive Estate Inventory

A fundamental step in the estate planning process is conducting a thorough inventory of the client’s assets and liabilities. As an accountant, your expertise in financial record-keeping and analysis makes you ideally suited to assist clients in this crucial task. Here’s how you can guide clients through a comprehensive estate inventory:

Categorizing Assets

Begin by helping clients categorize their assets. This typically includes:

- Real Estate: Primary residence, vacation homes, rental properties

- Financial Assets: Bank accounts, investment portfolios, retirement accounts (401(k)s, IRAs)

- Business Interests: Ownership stakes in companies, partnerships

- Personal Property: Vehicles, jewelry, art collections, antiques

- Digital Assets: Online accounts, cryptocurrencies, digital media libraries

For each category, encourage clients to provide detailed information. For real estate, this might include property addresses, approximate values, and any outstanding mortgages. For financial assets, gather account numbers, current balances, and beneficiary designations.

Identifying Liabilities

Equally important is a thorough accounting of liabilities. This includes:

- Mortgages

- Personal loans

- Credit card debts

- Business loans

- Tax obligations

Understanding the full scope of liabilities is crucial for accurate net worth calculations and for planning debt management strategies within the estate plan.

Documenting Important Information

Beyond just listing assets and liabilities, encourage clients to document important information related to each item. This might include:

- Location of physical assets

- Contact information for financial institutions

- Login credentials for digital assets (to be stored securely)

- Insurance policies covering various assets

This detailed documentation will be invaluable for executors or trustees managing the estate in the future.

Valuation Considerations

As an accountant, you can provide valuable insights into asset valuation. While some assets have clear market values, others may require professional appraisals. Advise clients on which assets might need expert valuation, such as:

- Closely held businesses

- Real estate in rapidly changing markets

- Unique collectibles or artwork

Accurate valuation is crucial not only for estate distribution but also for tax planning purposes.

Reviewing Beneficiary Designations

Part of the inventory process should include reviewing beneficiary designations on accounts such as life insurance policies, retirement accounts, and transfer-on-death accounts. These designations often supersede will instructions, making them a critical component of the estate plan.

Utilizing Technology for Inventory Management

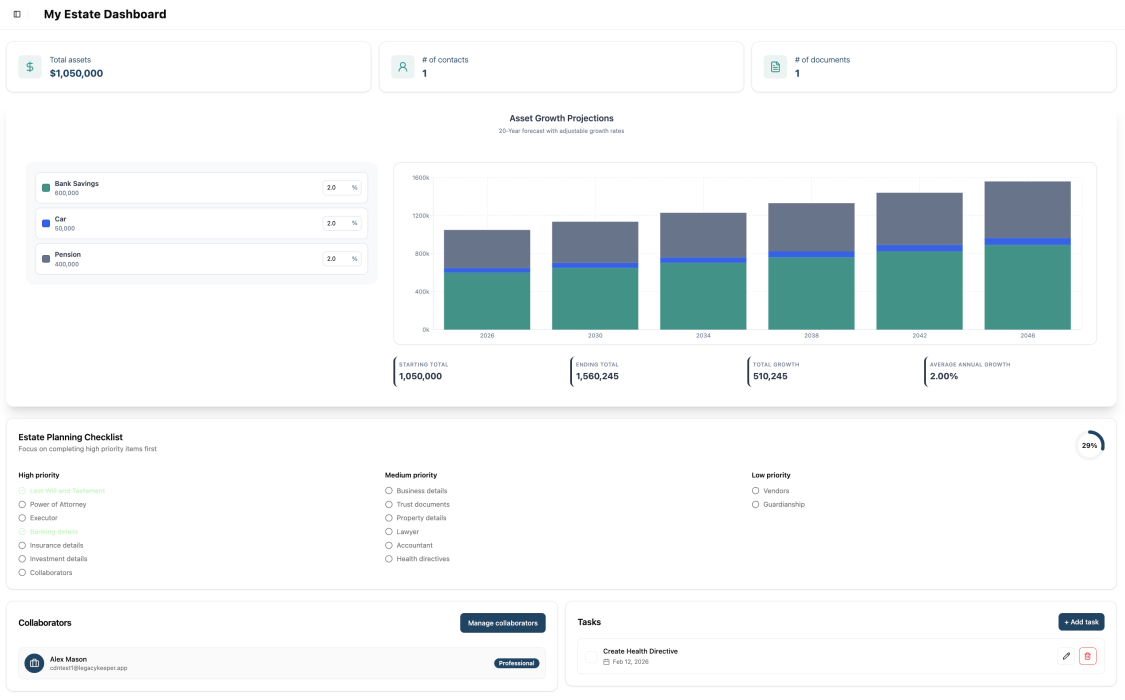

Consider recommending digital tools or apps designed for estate inventory management. These can help clients maintain an up-to-date record of their assets and liabilities. Some platforms, like LegacyKeeper.app, offer secure, user-friendly interfaces for organizing and updating estate information.

Periodic Review and Updates

Emphasize to clients the importance of regularly reviewing and updating their estate inventory. Significant life events, asset acquisitions or disposals, and market fluctuations can all impact the composition and value of their estate. Recommend an annual review at minimum, coinciding with their tax preparation if possible.

Collaboration with Other Professionals

In some cases, compiling a comprehensive estate inventory may require input from other professionals. Be prepared to collaborate with:

- Real estate agents for property valuations

- Business valuation experts for closely held companies

- Art appraisers for valuable collections

Your role as the accountant is to coordinate this information and ensure it’s accurately reflected in the overall estate inventory.

By guiding clients through a thorough estate inventory process, you provide them with a clear picture of their financial situation. This comprehensive overview serves as the foundation for all subsequent estate planning decisions, ensuring that strategies are tailored to the client’s specific circumstances and goals.

Developing Tax-Efficient Estate Planning Strategies

As an accountant, one of your most valuable contributions to the estate planning process is your expertise in tax laws and regulations. Developing tax-efficient strategies can significantly impact the value of the estate passed on to beneficiaries. Here’s how you can help clients minimize tax liabilities and maximize the value of their estates:

Understanding Current Estate Tax Laws

Stay informed about the latest estate tax laws, including federal and state-specific regulations. Key points to consider include:

- Federal estate tax exemption limits

- State-specific estate and inheritance tax rules

- Gift tax annual exclusion amounts

- Generation-skipping transfer tax considerations

Regularly update clients on changes in these laws and how they might affect their estate plans.

Lifetime Gifting Strategies

Advise clients on the benefits of lifetime gifting to reduce the taxable estate. This can include:

- Annual Exclusion Gifts: Recommend utilizing the annual gift tax exclusion to transfer wealth tax-free.

- Educational and Medical Gifts: Explain how direct payments for education or medical expenses are exempt from gift tax.

- Charitable Giving: Discuss options for charitable donations, including setting up charitable trusts or foundations.

Trust Structures for Tax Efficiency

Explore various trust structures that can offer tax advantages:

- Irrevocable Life Insurance Trusts (ILITs): These can remove life insurance proceeds from the taxable estate.

- Grantor Retained Annuity Trusts (GRATs): Useful for transferring appreciating assets with minimal gift tax consequences.

- Qualified Personal Residence Trusts (QPRTs): Can reduce the taxable value of a primary residence or vacation home.

Explain the pros and cons of each trust type and how they align with the client’s overall goals.

Business Succession Planning

For clients who own businesses, discuss tax-efficient strategies for transferring ownership:

- Family Limited Partnerships (FLPs): Can facilitate the transfer of business interests while maintaining control.

- Buy-Sell Agreements: Ensure these are structured to minimize tax implications for both the business and the owner’s estate.

- Employee Stock Ownership Plans (ESOPs): Consider as a tax-advantaged exit strategy for business owners.

Retirement Account Management

Advise on strategies for managing retirement accounts within the estate plan:

- Roth IRA Conversions: Discuss the potential long-term tax benefits for heirs.

- Required Minimum Distribution (RMD) Planning: Strategize on how to manage RMDs to minimize tax impact.

- Beneficiary Designations: Ensure these are optimized for tax efficiency, considering the new SECURE Act rules.

Asset Location and Portfolio Management

Guide clients on how to structure their investment portfolio for tax efficiency:

- Asset Location: Advise on which types of assets should be held in taxable versus tax-advantaged accounts.

- Tax-Loss Harvesting: Explain how this strategy can offset capital gains and reduce overall tax liability.

- Step-Up in Basis: Discuss the potential benefits of holding appreciated assets until death for a step-up in basis.

State Tax Considerations

Be aware of state-specific estate and inheritance tax laws:

- Domicile Planning: For clients with residences in multiple states, advise on establishing domicile in a tax-friendly state.

- State-Specific Exemptions: Understand and utilize any state-level estate tax exemptions or deductions.

Charitable Giving Strategies

Explore tax-efficient charitable giving options:

- Donor-Advised Funds: Discuss how these can provide immediate tax benefits while allowing for future charitable distributions.

- Charitable Remainder Trusts: Explain how these can provide income to the donor while ultimately benefiting a charity.

- Qualified Charitable Distributions: For clients over 70½, discuss using IRA funds for charitable giving to reduce taxable income.

Regular Review and Adjustment

Emphasize the importance of regularly reviewing and adjusting tax strategies:

- Annual Tax Planning Meetings: Schedule these to assess the impact of any life changes or new tax laws.

- Flexibility in Planning: Design strategies that can be adjusted as tax laws and personal circumstances change.

By implementing these tax-efficient strategies, you can help clients significantly reduce their estate tax burden and maximize the wealth transferred to their beneficiaries. Remember to tailor these strategies to each client’s unique situation and goals, and always consider the interplay between different tax considerations (income, estate, gift, and generation-skipping transfer taxes) to create a holistic and effective estate plan.

Assisting with Business Succession Planning

For clients who own businesses, integrating business succession planning into their overall estate plan is crucial. As their accountant, you play a vital role in ensuring a smooth transition of the business while minimizing tax implications and preserving family wealth. Here’s how you can guide clients through the business succession planning process:

Assessing the Current Business Structure

Begin by thoroughly evaluating the existing business structure:

- Legal Entity: Determine if the current legal structure (e.g., sole proprietorship, partnership, corporation) is optimal for succession.

- Ownership Distribution: Analyze the current ownership breakdown and any existing agreements among partners or shareholders.

- Management Structure: Assess the current management team and identify key personnel crucial for the business’s continuity.

Valuing the Business

Conduct or oversee a comprehensive business valuation:

- Financial Analysis: Review historical financial statements and project future cash flows.

- Market Comparison: Compare the business to similar companies in the industry.

- Asset Valuation: Assess the value of tangible and intangible assets.

A accurate valuation is crucial for fair distribution, tax planning, and potential sale negotiations.

Identifying Succession Options

Help clients explore various succession options:

- Family Transfer: Discuss the pros and cons of transferring the business to family members.

- Management Buyout: Consider the possibility of selling to existing management or employees.

- Third-Party Sale: Evaluate the option of selling the business to an external buyer.

- Gradual Transfer: Explore strategies for a phased transition of ownership and management.

Developing a Transition Timeline

Work with clients to create a realistic timeline for the succession process:

- Short-term Goals: Identify immediate steps to prepare the business for transition.

- Medium-term Objectives: Plan for gradual transfer of responsibilities and ownership.

- Long-term Vision: Align the succession plan with the client’s retirement and estate planning goals.

Structuring the Transfer

Advise on tax-efficient methods to structure the business transfer:

- Gifting Strategies: Utilize annual gift tax exclusions and lifetime exemptions.

- Sale to Intentionally Defective Grantor Trust (IDGT): Explain how this can facilitate a tax-efficient transfer.

- Employee Stock Ownership Plan (ESOP): Discuss the benefits of selling to employees through an ESOP.

- Installment Sales: Explore the tax advantages of selling the business over time.

Addressing Funding Needs

Help clients plan for the financial aspects of succession:

- Buy-Sell Agreements: Assist in drafting and funding buy-sell agreements.

- Life Insurance: Advise on using life insurance to fund buyouts or equalize inheritances.

- Retirement Planning: Ensure the succession plan aligns with the owner’s retirement income needs.

Training and Mentoring Successors

Emphasize the importance of preparing the next generation of leadership:

- Skills Assessment: Identify areas where potential successors need development.

- Training Programs: Recommend or help design training programs for successors.

- Gradual Responsibility Transfer: Advise on a phased approach to transferring management responsibilities.

Minimizing Tax Impact

Develop strategies to minimize tax liabilities during the transition:

- Estate Freeze Techniques: Explain methods to lock in the current value of the business for estate tax purposes.

- Charitable Strategies: Explore options like charitable remainder trusts to reduce tax burden.

- Deferred Compensation Plans: Discuss how these can provide tax benefits for both the business and the retiring owner.

Addressing Family Dynamics

Navigate the sensitive aspects of family business succession:

- Family Meetings: Encourage open communication among family members about the succession plan.

- Fairness Considerations: Address how to treat active vs. non-active family members in the business.

- Conflict Resolution: Suggest mechanisms for resolving potential disputes during and after the transition.

Integrating with Personal Estate Plan

Ensure the business succession plan aligns with the client’s overall estate plan:

- Will and Trust Coordination: Align business succession with provisions in wills and trusts.

- Beneficiary Designations: Review and update beneficiary designations on business-related accounts and policies.

- Power of Attorney: Advise on the importance of having a business power of attorney in place.

Regular Review and Updates

Stress the importance of regularly reviewing and updating the succession plan:

- Annual Reviews: Schedule yearly check-ins to assess progress and make necessary adjustments.

- Trigger Events: Identify events (e.g., changes in tax laws, family dynamics, or business performance) that necessitate plan revisions.

By guiding clients through these aspects of business succession planning, you help ensure that their life’s work is preserved and transitioned effectively. This process not only secures the business’s future but also plays a crucial role in achieving the client’s overall estate planning objectives.

Navigating Complex Family Dynamics in Estate Planning

Estate planning often involves navigating complex family dynamics, which can significantly impact the planning process and the implementation of the estate plan. As an accountant, your role extends beyond financial advice to helping clients address these sensitive family issues. Here’s how you can assist clients in managing family dynamics within the context of estate planning:

Understanding Family Structures

Begin by gaining a comprehensive understanding of the client’s family structure:

- Blended Families: Be aware of the challenges in planning for step-children and multiple marriages.

- Multigenerational Families: Consider the needs and expectations of different generations.

- Family Businesses: Recognize the interplay between business and personal relationships.

Facilitating Open Communication

Encourage clients to foster open communication within the family:

- Family Meetings: Suggest holding family meetings to discuss estate planning goals and decisions.

- Mediation: Recommend professional mediation services for difficult conversations if necessary.

- Transparency: Advise on the level of information to share with family members at different stages.

Addressing Fairness and Equality

Help clients navigate the often-tricky balance between fairness and equality:

- Equal vs. Equitable Distribution: Discuss the differences and help clients decide which approach aligns with their goals.

- Non-Monetary Factors: Consider how to account for non-financial contributions by family members.

- Special Needs Planning: Address the unique requirements of family members with special needs or disabilities.

Managing Expectations

Assist clients in managing family members’ expectations:

- Clear Communication: Encourage clients to clearly communicate their intentions to avoid surprises.

- Explaining Decisions: Help clients articulate the reasoning behind their estate planning choices.

- Gradual Disclosure: Advise on whether a phased approach to sharing information might be beneficial.

Addressing Potential Conflicts

Help clients anticipate and mitigate potential family conflicts:

- Identifying Trigger Points: Recognize issues that might lead to disputes among family members.

- Conflict Resolution Clauses: Suggest including mediation or arbitration clauses in estate documents.

- No-Contest Clauses: Discuss the pros and cons of including no-contest provisions in wills or trusts.

Balancing Control and Independence

Guide clients in finding the right balance between maintaining control and fostering independence:

- Trust Structures: Explain how different trust structures can provide varying levels of control and flexibility.

- Staged Inheritance: Discuss the option of distributing inheritances in stages based on age or milestones.

- Financial Education: Recommend programs or resources to help heirs develop financial literacy.

Addressing Unequal Financial Situations

Help clients navigate situations where family members have significantly different financial needs or resources:

- Lifetime Gifting: Discuss strategies for addressing financial imbalances through lifetime gifts.

- Separate Share Trusts: Explain how these can be used to provide tailored support for different beneficiaries.

- Incentive Trusts: Explore the use of incentive provisions to encourage certain behaviors or achievements.

Dealing with Estranged Family Members

Provide guidance on handling estranged or problematic family relationships:

- Legal Obligations: Inform clients about any legal requirements regarding disinheritance.

- Documentation: Stress the importance of clearly documenting decisions regarding estranged family members.

- Alternative Solutions: Explore options like leaving a token inheritance or creating a separate trust for estranged members.

Incorporating Family Values and Legacy

Help clients integrate their values and desired legacy into the estate plan:

- Ethical Wills: Introduce the concept of ethical wills to communicate values and life lessons.

- Family Philanthropy: Discuss options for involving family members in charitable giving decisions.

- Family History Preservation: Suggest ways to preserve and share family history and traditions.

Addressing International Family Issues

For clients with international family connections, consider:

- Cross-Border Estate Planning: Advise on the complexities of planning across different jurisdictions.

- Cultural Sensitivities: Be aware of and respect cultural differences in approaches to inheritance and family roles.

- Currency and Tax Implications: Address the challenges of transferring assets across international borders.

Recommending Professional Support

Know when to recommend additional professional support:

- Family Therapists: Suggest family therapy to address deep-seated issues affecting estate planning.

- Wealth Psychologists: Introduce the concept of wealth psychology to help families navigate the emotional aspects of wealth transfer.

- Specialized Legal Counsel: Recommend attorneys with expertise in complex family situations when necessary.

By addressing these family dynamics thoughtfully and proactively, you can help clients create estate plans that not only meet their financial objectives but also preserve family harmony and reflect their values. Remember that every family is unique, and solutions should be tailored to each client’s specific situation and goals.

Leveraging Technology in Estate Planning For Accountants

In today’s digital age, technology plays an increasingly important role in estate planning. As an accountant, embracing and leveraging these technological advancements can significantly enhance your ability to assist clients with their estate planning needs. Here’s how you can incorporate technology into your estate planning services:

Digital Asset Management

Help clients identify and manage their digital assets:

- Inventory Tools: Recommend software for creating and maintaining a digital asset inventory.

- Password Managers: Advise on secure password management solutions for storing login credentials.

- Digital Legacy Services: Introduce services that help manage online accounts after death.

Estate Planning For Accountants Software

Utilize specialized estate planning software:

- Document Preparation: Use software to draft basic estate planning documents.

- Scenario Modeling: Employ tools that allow for modeling different estate planning scenarios.

- Collaboration Platforms: Implement software that facilitates collaboration with clients and other professionals.

Online Secure Document Storage

Recommend secure online storage solutions:

- Cloud Storage: Advise on reputable cloud storage services for important documents.

- Encrypted File Sharing: Use encrypted file-sharing platforms to exchange sensitive information securely.

- Digital Vaults: Introduce digital vault services designed specifically for estate planning documents.

Virtual Meeting Platforms

Embrace virtual meeting technologies:

- Video Conferencing: Utilize video conferencing tools for remote client meetings and consultations.

- Screen Sharing: Use screen sharing features to review documents and financial models with clients.

- Recording Capabilities: Consider recording meetings (with client consent) for future reference.

Financial Planning and Projection Tools

Leverage advanced financial planning software:

- Cash Flow Modeling: Use tools to project long-term cash flows and estate growth.

- Tax Impact Analysis: Employ software that can model the tax implications of different estate planning strategies.

- Monte Carlo Simulations: Utilize tools that can run simulations to assess the robustness of estate plans under various scenarios.

Client Portals

Implement client portals for enhanced communication and document sharing:

- Secure Messaging: Use portals with built-in secure messaging features.

- Document Upload/Download: Allow clients to securely upload and download important documents.

- Progress Tracking: Provide clients with the ability to track the progress of their estate planning process.

Digital Signature Solutions

Adopt digital signature technology:

- E-Signature Platforms: Implement e-signature solutions for document execution.

- Compliance Features: Ensure the chosen platform complies with legal requirements for document signing.

- Audit Trails: Utilize solutions that provide detailed audit trails for all signed documents.

AI and Machine Learning Tools

Explore the potential of AI and machine learning in estate planning:

- Data Analysis: Use AI-powered tools to analyze large volumes of financial data.

- Risk Assessment: Employ machine learning algorithms to identify potential risks in estate plans.

- Automated Reporting: Implement AI-driven reporting tools for generating comprehensive estate planning reports.

Mobile Applications

Recommend and utilize mobile apps for estate planning:

- Asset Tracking Apps: Suggest apps that help clients track and update their asset information on-the-go.

- Estate Planning Education Apps: Recommend educational apps that can help clients understand estate planning concepts.

- Notification Systems: Use apps that provide reminders for important estate planning tasks and deadlines.

Blockchain Technology

Stay informed about the potential applications of blockchain in estate planning:

- Smart Contracts: Understand how smart contracts could be used for executing certain aspects of estate plans.

- Asset Verification: Explore blockchain’s potential for verifying ownership and transferring digital assets.

- Immutable Records: Consider the benefits of blockchain for creating tamper-proof records of estate planning documents.

Cybersecurity Measures

Implement robust cybersecurity practices:

- Encryption: Use strong encryption for all sensitive client data.

- Multi-Factor Authentication: Implement multi-factor authentication for accessing client information.

- Regular Security Audits: Conduct periodic security audits of your technology systems.

Integration with LegacyKeeper.app

Explore the features of LegacyKeeper.app:

- Comprehensive Asset Tracking: Utilize the app’s features for detailed asset inventory and management.

- Collaborative Planning: Leverage the app’s collaborative tools to work seamlessly with clients and other professionals.

- Secure Information Sharing: Use the app’s secure sharing features to exchange sensitive information with clients.

By effectively leveraging these technological tools and platforms, you can streamline the estate planning for accountants process, enhance security, and provide more comprehensive and efficient services to your clients. Remember to stay updated on the latest technological advancements in the field and always prioritize data security and client confidentiality when adopting new tools.

Estate Planning For Accountants: Collaborating with Legal Professionals

Effective estate planning for accountants often requires a collaborative effort between accountants and legal professionals. As an accountant, your role in this collaboration is crucial, bringing financial expertise to complement the legal knowledge of attorneys. Here’s how you can effectively work with legal professionals to provide comprehensive estate planning services to your clients:

Establishing Professional Relationships

Build a network of trusted legal professionals:

- Networking Events: Attend local bar association events or estate planning seminars to meet attorneys.

- Professional Associations: Join professional associations that include both accountants and attorneys.

- Referral Partnerships: Develop mutual referral relationships with estate planning attorneys.

Defining Roles and Responsibilities

Clearly delineate the roles of accountants and attorneys in the estate planning process:

- Scope of Work: Clearly define which aspects of the plan you’ll handle versus the attorney.

- Communication Protocol: Establish a clear communication protocol for sharing information and updates.

- Client Confidentiality: Ensure both parties understand and respect client confidentiality boundaries.

Sharing Financial Information

Provide comprehensive financial data to support legal planning:

- Asset Summaries: Prepare detailed summaries of client assets and liabilities.

- Tax Projections: Offer tax projections under various estate planning scenarios.

- Business Valuations: Share business valuation reports for clients with business interests.

Interpreting Tax Implications Is Key To Estate Planning For Accountants

Offer insights on the tax implications of various legal strategies:

- Tax Analysis: Provide analysis of how different legal structures might impact the client’s tax situation.

- Income Tax Considerations: Highlight income tax issues that may arise from certain estate planning decisions.

- State-Specific Tax Issues: Inform attorneys about state-specific tax considerations that may affect the plan.

Reviewing Legal Documents

Assist in reviewing estate planning documents from a financial perspective:

- Trust Provisions: Review trust documents to ensure they align with the client’s financial goals.

- Asset Titling: Verify that asset titling recommendations in legal documents are financially sound.

- Beneficiary Designations: Cross-check beneficiary designations with the overall estate plan.

Implementing the Plan

Collaborate on the implementation of the estate plan:

- Asset Transfers: Assist with the financial aspects of transferring assets into trusts or other entities.

- Business Restructuring: Work together on implementing business succession plans.

- Charitable Giving Strategies: Coordinate on setting up and funding charitable giving vehicles.

Ongoing Monitoring and Updates

Partner with attorneys for regular plan reviews and updates:

- Annual Reviews: Conduct joint annual reviews with the attorney to assess the plan’s effectiveness.

- Legislative Changes: Keep attorneys informed of tax law changes that may impact estate plans.

- Life Changes: Alert attorneys to significant changes in the client’s financial situation that may necessitate plan updates.

Addressing Complex Scenarios

Collaborate closely on complex estate planning scenarios:

- International Assets: Work together to address issues related to foreign assets or beneficiaries.

- Special Needs Planning: Combine expertise to create effective plans for clients with special needs dependents.

- Blended Families: Collaborate on strategies for equitable planning in blended family situations.

Educating Clients About Estate Planning As An Accountant

Work together to educate clients on accounting estate planning concepts:

- Joint Presentations: Conduct joint client seminars on estate planning topics.

- Complementary Explanations: Provide financial explanations to complement the attorney’s legal explanations.

- Client Questions: Coordinate responses to client questions to ensure consistent messaging.

Utilizing Technology In Estate Planning For Accountants

Leverage technology for efficient collaboration:

- Shared Platforms: Use secure, shared platforms for document storage and collaboration.

- Virtual Meetings: Conduct joint virtual meetings with clients when in-person

References: Estate Planning For Accountants

- Crow Estate Planning & Probate: Here is Why an Accountant IsImportant In Dealing With EstateMatters

- Canadian Estate Planning: The Role Of An Accountant In Estate Planning

- Anthem: The Accountant’s Role In Estate Planning & Administration

- CPA Practice Advisor: Estate Planning: A Guide for Accountants

- Legacy Planning Law Group: The Role of a CPA in Estate Planning

- Legacy Keeper: Estate Planning For Financial Advisors

Leave a Reply