When a loved one passes away, dealing with the emotional toll is challenging enough without worrying about calculating taxes On Death In B.C.. In addition, the complexities of managing their estate and understanding the associated tax implications can feel overwhelming. If you’re navigating this difficult terrain in British Columbia, you’re likely wondering about the taxes that apply when someone dies. While there’s no direct “inheritance tax” in B.C., there are still important financial considerations to remember. This guide will walk you through calculating taxes on death in British Columbia, helping you understand what to expect and how to prepare.

Death and taxes may be inevitable, but with the right knowledge and planning, you can minimize the impact on your loved ones’ inheritance. Let’s dive into the intricacies of B.C. taxes on death, breaking down complex concepts into digestible information that will empower you to make informed decisions during this challenging time.

The passing of a family member or friend brings a whirlwind of emotions and responsibilities. Among these is settling their financial affairs, which includes addressing any tax obligations. In British Columbia, while beneficiaries don’t face direct taxation on their inheritances, the deceased’s estate may be subject to various taxes and fees before assets can be distributed. Understanding these financial implications is crucial for effective estate planning and management.

As we explore the landscape of B.C. taxes on death, we’ll cover everything from income tax considerations to probate fees, capital gains, and strategies for minimizing the tax burden. Whether you’re planning for the future or dealing with a recent loss, this guide will provide you with the knowledge you need to navigate the financial aspects of death in British Columbia with confidence and clarity.

Understanding the Basics of Calculating Taxes On Death In B.C.

When someone passes away in British Columbia, their estate becomes responsible for settling any outstanding tax obligations. Unlike some jurisdictions, B.C. doesn’t impose a specific “death tax” or inheritance tax on beneficiaries. However, this doesn’t mean the deceased’s assets are exempt from taxation.

The Canada Revenue Agency (CRA) treats the deceased as having disposed of all their assets at fair market value immediately before death. This concept, known as “deemed disposition,” can trigger various tax implications for the estate. It’s essential to understand that while heirs don’t pay taxes directly on their inheritance, the overall value of what they receive may be reduced by the taxes the estate must pay.

In British Columbia, there are two primary financial considerations when someone dies:

- Income taxes on the deceased’s final tax return

- Probate fees on the estate’s assets

Let’s break these down further to give you a clearer picture of what to expect.

Income Tax Obligations

The estate executor is responsible for filing the deceased’s final tax return. This return must include all income earned up to the date of death, including:

- Employment income

- Pension payments

- Investment income

- Capital gains from deemed disposition of assets

It’s important to note that some income received after death, such as dividends or interest, may need to be reported on a separate rights or things return.

Probate Fees in British Columbia

Probate is the legal process of validating a will and authorizing the executor to manage the estate. In B.C., probate fees are calculated based on the gross value of the estate’s assets that pass through probate. As of 2023, the fee structure is as follows:

- No fee for estates valued under $25,000

- $200 base fee for estates valued between $25,000 and $50,000

- $200 plus 0.6% on the portion of the estate between $25,000 and $50,000

- $200 plus 1.4% on the portion of the estate exceeding $50,000

Understanding these basic principles sets the foundation for calculating B.C. taxes on death. The following sections will delve deeper into specific scenarios and strategies to help you navigate this complex landscape. Remember that moving assets out of the estate will lower the final tax return and the probate fees.

Deemed Disposition: The Cornerstone of Estate Taxation

At the heart of calculating B.C. taxes on death lies the concept of deemed disposition. This principle, established by the Income Tax Act, assumes that the deceased has sold all their capital property at fair market value immediately before death. While no actual sale occurs, this theoretical transaction can trigger significant tax implications for the estate.

How Deemed Disposition Works

When a person passes away, the CRA considers their assets to have been “disposed of” at their current market value. This applies to most types of property, including:

- Real estate (excluding principal residence)

- Stocks and bonds

- Mutual funds

- Business assets

- Collectibles and valuable personal property

The difference between the asset’s original purchase price (adjusted cost base) and its fair market value at the time of death is treated as a capital gain. Half of this gain is then added to the deceased’s income for the year of death and taxed accordingly.

Exceptions to Deemed Disposition

While deemed disposition applies to most assets, there are some notable exceptions:

- Principal Residence: The capital gains on a primary home are typically exempt from taxation.

- Registered Accounts: RRSPs and RRIFs are treated differently and are generally considered to be fully withdrawn at death.

- Spousal Transfers: Assets transferred to a surviving spouse or common-law partner may be eligible for a tax-deferred rollover.

Understanding these exceptions can be crucial in estate planning and minimizing the tax burden on the deceased’s estate.

Impact on Estate Valuation

Deemed disposition can significantly affect the overall value of an estate. The resulting capital gains tax can be substantial for assets that have appreciated substantially over time. This is why it’s essential to clearly understand the current market value of all assets when calculating potential taxes on death in B.C.

By grasping the concept of deemed disposition and its implications, you’ll be better equipped to anticipate potential tax liabilities and plan accordingly. In the next section, we’ll explore how to calculate capital gains and losses in the context of estate taxation.

Calculating Capital Gains and Losses

When it comes to B.C. taxes on death, understanding how to calculate capital gains and losses is crucial. These calculations form a significant part of the deceased’s final tax return and can greatly impact the estate’s overall tax liability.

What Constitutes a Capital Gain or Loss?

A capital gain occurs when an asset is deemed to have been sold for more than its adjusted cost base (ACB). Conversely, a capital loss happens when the deemed sale price exceeds the ACB. The ACB includes the original purchase price plus any costs associated with acquiring or improving the asset.

The 50% Rule

In Canada, only 50% of capital gains are taxable. If an asset has appreciated, half of that increase will be added to the deceased’s income for the year of death. For example:

- Original purchase price of a rental property: $200,000

- Fair market value at death: $300,000

- Capital gain: $100,000

- Taxable capital gain: $50,000 (50% of $100,000)

Calculating Gains and Losses for Different Asset Types

Different types of assets may have specific rules for calculating capital gains:

- Real Estate:

- Calculate the difference between the fair market value and the ACB

- Consider any capital improvements made to the property

- Stocks and Securities:

- Use the fair market value on the date of death

- Account for any commissions or fees in the ACB

- Personal Property:

- Only applicable for items worth over $1,000

- Special rules may apply for collections or sets

Offsetting Gains with Losses

Capital losses can be used to offset capital gains, potentially reducing the overall tax burden. In the context of a final tax return:

- Losses can be applied against gains in the year of death

- Unused losses can be carried back to offset gains in the three preceding years

- Any remaining losses can be used to reduce other income on the final return

The Importance of Accurate Valuation

Obtaining accurate valuations for assets is critical when calculating capital gains and losses. Professional appraisals may be necessary for unique or high-value items to ensure proper reporting and avoid potential disputes with tax authorities.

By accurately calculating capital gains and losses, you can better estimate the potential tax implications for an estate in British Columbia. This knowledge is invaluable for estate planning and executors managing a deceased person’s final tax obligations.

Registered Accounts: Special Considerations

When calculating B.C. taxes on death, registered accounts like Registered Retirement Savings Plans (RRSPs) and Registered Retirement Income Funds (RRIFs) require special attention. These accounts are treated differently from other assets and can have significant tax implications for the estate.

Deemed Withdrawal of RRSPs and RRIFs

Upon death, the full value of RRSPs and RRIFs is considered to be withdrawn immediately before the account holder’s passing. This means:

- The entire balance is included as income on the deceased’s final tax return

- This can result in a substantial tax bill, especially for large accounts

Tax Deferral Options

There are ways to defer taxes on registered accounts, depending on who inherits them:

- Spousal Rollover:

- If the beneficiary is a spouse or common-law partner, the funds can be transferred to their own RRSP or RRIF tax-free

- Taxes are deferred until the surviving spouse makes withdrawals or passes away

- Financially Dependent Children or Grandchildren:

- In certain cases, funds can be transferred to a dependent child or grandchild’s RRSP, RRIF, or used to purchase an annuity

- This can spread the tax burden over a longer period

Tax-Free Savings Accounts (TFSAs)

TFSAs are treated more favorably in terms of taxation at death:

- The value of the TFSA at the date of death can be transferred to beneficiaries tax-free

- Any growth in the account after the date of death may be taxable to the beneficiaries

Strategies for Minimizing Tax Impact

To reduce the potential tax burden on registered accounts:

- Gradual Withdrawal:

- Consider making strategic withdrawals during retirement to spread out the tax liability

- This can prevent a large lump sum from being taxed at a high rate upon death

- Beneficiary Designations:

- Ensure beneficiaries are properly designated on registered accounts

- This can facilitate smoother transfers and potentially reduce probate fees

- Pension Income Splitting:

- For couples, using pension income splitting during retirement can help balance income levels

- This strategy can lead to a lower overall tax rate when one spouse passes away

Reporting Requirements

Executors should be aware of specific reporting requirements for registered accounts:

- T4RSP or T4RIF slips must be issued for the deemed withdrawal

- These amounts need to be included on the deceased’s final tax return

Understanding the unique treatment of registered accounts is crucial when calculating B.C. taxes on death. Proper planning and beneficiary designations can help minimize the tax impact and ensure a smoother transfer of these valuable assets to heirs.

Probate Fees and Estate Administration

While not technically a tax, probate fees are an important consideration when calculating the overall financial impact of death in British Columbia. Probate is the legal process of validating a will and authorizing the executor to manage and distribute the estate. Understanding how probate fees work and strategies to minimize them can help preserve more of the estate for beneficiaries.

Calculating Probate Fees in B.C.

Probate fees in British Columbia are based on the gross value of the estate assets that pass through probate. As of 2023, the fee structure is:

- No fee for estates valued under $25,000

- $200 base fee for estates valued at $25,000 or more

- Plus 0.6% on the portion of the estate between $25,000 and $50,000

- Plus 1.4% on the portion of the estate exceeding $50,000

For example, an estate valued at $500,000 would incur probate fees of approximately $6,650.

Assets Subject to Probate

Not all assets are subject to probate. Generally, probate applies to:

- Real estate solely in the deceased’s name

- Bank accounts solely in the deceased’s name

- Investments and securities not held jointly or without named beneficiaries

Assets That May Avoid Probate

Certain assets can potentially bypass the probate process:

- Jointly held property with right of survivorship

- Registered accounts (RRSPs, RRIFs, TFSAs) with named beneficiaries

- Life insurance policies with named beneficiaries

- Assets held in trusts

Strategies to Minimize Probate Fees

To reduce probate fees and simplify estate administration:

- Joint Ownership:

- Consider holding assets jointly with right of survivorship

- Be aware of potential pitfalls, such as exposure to creditors or family law claims

- Beneficiary Designations:

- Ensure registered accounts and insurance policies have up-to-date beneficiary designations

- This allows these assets to pass outside of the estate

- Inter-Vivos Trusts:

- Setting up a living trust can help certain assets avoid probate

- Consult with a legal professional to determine if this strategy is appropriate

- Multiple Wills:

- In some cases, using multiple wills (one for assets requiring probate and one for those that don’t) can be effective

- This strategy requires careful legal planning

The Role of the Executor

The executor plays a crucial role in estate administration:

- Gathering and valuing estate assets

- Applying for probate if necessary

- Paying debts and taxes

- Distributing assets to beneficiaries

Executors should be aware of their responsibilities and the potential personal liability they may face if estate administration is not handled correctly.

Understanding probate fees and estate administration is essential for estate planning and executors managing a deceased person’s affairs. By implementing strategies to minimize probate fees where appropriate, you can help ensure more of the estate’s value is preserved for beneficiaries.

Principal Residence Exemption and Other Tax-Free Transfers

When calculating B.C. taxes on death, it’s crucial to understand which assets may be exempt from taxation or eligible for tax-free transfers. These exemptions can significantly reduce the overall tax burden on an estate.

Principal Residence Exemption

One of the most valuable tax exemptions in Canada is the principal residence exemption. This allows homeowners to avoid paying capital gains tax on the increase in value of their primary residence. Key points to remember:

- Only one property can be designated as a principal residence for any given year

- The exemption can apply to a house, condo, cottage, or even a houseboat

- The property must be ordinarily inhabited by the taxpayer or their family members

When someone passes away, their estate can claim the principal residence exemption on their final tax return, potentially eliminating a significant tax liability.

Calculating the Principal Residence Exemption

The calculation for the principal residence exemption takes into account:

- The number of years the property was designated as the principal residence

- The total number of years the property was owned

Depending on the circumstances, this can result in a full or partial exemption.

Other Tax-Free Transfers

Several other types of transfers can occur without triggering immediate tax consequences:

- Spousal Rollover:

- Assets can be transferred to a surviving spouse or common-law partner on a tax-deferred basis

- This includes most types of property, including real estate and investments

- Farm or Fishing Property:

- Special rules allow for the tax-deferred transfer of qualified farm or fishing property to children or grandchildren

- Charitable Donations:

- Donations made through a will or by designation can provide tax credits to offset other taxes payable by the estate

Lifetime Capital Gains Exemption

While not strictly a tax-free transfer at death, the Lifetime Capital Gains Exemption can be valuable for estate planning:

- Applies to qualified small business corporation shares and certain farm or fishing property

- As of 2023, the lifetime limit is $971,190 for small business shares and $1 million for farm or fishing property

- Any unused exemption can be claimed on the deceased’s final tax return

Strategies for Maximizing Tax-Free Transfers

To make the most of these exemptions and tax-free transfers:

- Proper Documentation:

- Keep detailed records of property ownership and use

- Document any improvements or renovations to support cost base calculations

- Strategic Property Designation:

- Consider which property to designate as the principal residence if multiple properties are owned

- This decision can have significant tax implications

- Estate Planning:

- Work with professionals to structure your estate in a way that maximizes tax-free transfers

- Consider the use of trusts or other vehicles to achieve your goals

- Regular Review:

- Periodically review your estate plan to ensure it aligns with current tax laws and your circumstances

Understanding and utilizing these tax exemptions and tax-free transfer options can greatly reduce the B.C. taxes on death for an estate. By planning and seeking professional advice, you can help ensure that more of your assets are preserved for your beneficiaries.

Strategies for Minimizing Estate Taxes

While B.C. taxes on death are inevitable to some extent, several strategies can help minimize the overall tax burden on an estate. By implementing these approaches, you can potentially preserve wealth for your beneficiaries.

Lifetime Gifting

One effective way to reduce estate taxes is to gift assets during your lifetime:

- Gifts made during your lifetime are generally not taxable to the recipient

- This can reduce the size of your estate and potentially lower probate fees

- Be aware of attribution rules for gifts to spouses or minor children

Use of Trusts

Trusts can be powerful tools for estate planning and tax minimization:

- Inter-Vivos Trusts:

- Assets transferred to a living trust may avoid probate

- Can provide ongoing control and potential tax benefits

- Testamentary Trusts:

- Created through a will, these trusts can provide income splitting opportunities for beneficiaries

- Useful for providing for minor children or beneficiaries with special needs

Strategic Use of Life Insurance

Life insurance can play a crucial role in estate planning:

- Death benefits are generally tax-free to the beneficiary

- Can provide liquidity to pay estate taxes without selling assets

- Consider using an Immediate Financing Arrangement (IFA) to fund premiums tax-efficiently

Charitable Giving

Incorporating charitable donations into your estate plan can provide tax benefits:

- Donations made through a will generate tax credits that can offset other taxes

- Consider donating appreciated securities to eliminate capital gains tax

Income Splitting Strategies

Balancing income between spouses can lead to tax savings:

- Use pension income splitting during retirement

- Consider spousal RRSPs to equalize retirement income

Corporate Estate Freezes

For business owners, an estate freeze can cap the tax liability on future growth:

- Allows for the transfer of future growth to the next generation

- Can utilize the Lifetime Capital Gains Exemption of multiple family members

Regular Review and Updating

Estate planning is not a one-time event:

- Regularly review and update your will and estate plan

- Stay informed about changes in tax laws that may affect your strategy

Professional Advice

Working with experienced professionals is crucial:

- Consult with estate lawyers, tax specialists, and financial advisors

- Ensure your plan is tailored to your specific circumstances and goals

Consideration of U.S. Assets

If you own U.S. property or investments:

- Be aware of potential U.S. estate tax implications

- Consider specialized structures or insurance products to manage this exposure

Maximizing Tax-Deferred Accounts

Strategically using tax-deferred accounts can help manage your tax liability:

- Contributions to RRSPs, TFSAs, and other tax-advantaged accounts

- Consider the timing of withdrawals to minimize overall tax impact

By combining these strategies, you can work towards minimizing B.C. taxes on death and preserving more of your estate for your beneficiaries. Remember that estate planning is a complex area, and what works best will depend on your circumstances. Always consult with qualified professionals to ensure your strategy aligns with current laws and your personal goals.

The Role of the Executor in Managing Estate Taxes

The executor of an estate plays a crucial role in managing and minimizing B.C. taxes on death. This responsibility involves a range of duties, from filing final tax returns to making strategic decisions that can impact the overall tax liability of the estate.

Key Responsibilities of the Executor

When it comes to managing estate taxes, the executor’s primary duties include:

- Gathering and Valuing Assets:

- Compile a comprehensive inventory of the deceased’s assets

- Obtain professional appraisals where necessary

- Filing Tax Returns:

- Prepare and file the deceased’s final tax return

- File any necessary estate tax returns

- Paying Debts and Taxes:

- Ensure all outstanding debts and taxes are paid from estate funds

- Obtain clearance certificates from tax authorities

- Distributing Assets:

- Distribute remaining assets to beneficiaries according to the will or intestacy laws

Strategic Decisions for Tax Minimization

Executors can make several strategic choices to reduce the estate’s tax burden potentially:

- Electing the Right Tax Year:

- Choose the most advantageous fiscal period for the estate

- Deciding on Income Allocations:

- Determine whether to allocate certain income to the estate or beneficiaries

- Claiming Capital Losses:

- Decide whether to carry back capital losses to offset gains in previous years

- Making Charitable Donations:

- Consider making donations to utilize available tax credits

Dealing with Complex Assets

Executors may need to handle various types of assets with specific tax implications:

- Business Interests: Valuation and potential application of the Lifetime Capital Gains Exemption

- Foreign Assets: Navigating international tax laws and reporting requirements

- Registered Accounts: Managing the tax implications of RRSPs, RRIFs, and TFSAs

Seeking Professional Assistance

Given the complexities involved, executors should consider seeking professional help.

- Tax Specialists: For complex tax situations and strategy development

- Legal Advisors: To navigate probate and ensure compliance with estate laws

- Financial Advisors: For assistance with asset valuation and investment decisions

Potential Personal Liability

Executors should be aware of their potential personal liability:

- Ensure all taxes are paid before distributing assets to beneficiaries

- Obtain clearance certificates from tax authorities to limit personal risk

Communication with Beneficiaries

Clear communication is essential:

- Keep beneficiaries informed about the estate administration process

- Explain any tax implications that may affect their inheritances

Record Keeping

Maintaining detailed records is crucial:

- Keep all receipts, statements, and correspondence related to the estate

- Document all decisions and actions taken in managing the estate

Timeline Considerations

Executors must be mindful of important deadlines:

- File the final tax return by April 30th of the year following death or six months after the date of death, whichever is later

- Be aware of the timeline for obtaining probate and distributing assets

Executors can play a significant role in minimizing B.C. taxes on death and ensuring the smooth administration of the estate by understanding and effectively managing these responsibilities. The complexities involved often make professional assistance invaluable in navigating this process successfully.

Common Mistakes to Avoid When Calculating Estate Taxes

Executors and estate planners should be aware of several common pitfalls when dealing with B.C. taxes on death. Avoiding these mistakes can help ensure accurate tax calculations and prevent unnecessary financial and legal complications.

Overlooking Assets

One of the most frequent errors is failing to account for all assets:

- Forgetting about digital assets like cryptocurrencies or online accounts

- Overlooking foreign property or investments

- Neglecting to include life insurance policies owned by the deceased

Incorrect Valuation of Assets

Improper valuation can lead to significant tax discrepancies:

- Relying on outdated appraisals for real estate or valuable personal property

- Failing to account for accrued interest or dividends up to the date of death

- Misunderstanding the valuation rules for private company shares

Mishandling Registered Accounts

Mistakes with RRSPs, RRIFs, and TFSAs can be costly:

- Failing to explore tax-deferral options for eligible beneficiaries

- Overlooking the potential for pension income splitting in the year of death

- Misunderstanding the tax implications of beneficiary designations

Misapplying the Principal Residence Exemption

The principal residence exemption can be complex:

- Incorrectly designating multiple properties as principal residences

- Failing to properly calculate the exemption for properties owned for only part of the holding period

- Overlooking the potential to designate a cottage or vacation property as a principal residence

Neglecting Tax Loss Selling Opportunities

Failing to utilize capital losses can result in missed tax savings:

- Not considering the option to carry back capital losses to offset gains in previous years

- Overlooking the potential to trigger losses on investments to offset gains elsewhere in the estate

Improper Handling of Charitable Donations

Mistakes with charitable giving can reduce potential tax benefits:

- Failing to make optimal use of charitable donation tax credits

- Not considering the benefits of donating appreciated securities instead of cash

Misunderstanding Probate Fee Calculations

Errors in probate fee calculations can lead to overpayment:

- Including assets that don’t require probate in the fee calculation

- Failing to explore strategies to minimize probate fees, such as multiple wills or inter-vivos trusts

Neglecting Foreign Tax Implications

For estates with international assets, overlooking foreign tax laws can be costly:

- Failing to consider U.S. estate tax for Canadian residents with U.S. assets

- Overlooking foreign reporting requirements for overseas accounts or property

Mishandling the Tax-Free Savings Account (TFSA)

TFSAs require special attention:

- Not understanding the tax implications of TFSA transfers to beneficiaries

- Failing to report TFSA information on the deceased’s final return properly

Incorrect Timing of Estate Distributions

Distributing assets too quickly can create problems:

- Paying out beneficiaries before all tax liabilities are settled

- Failing to obtain clearance certificates from tax authorities before final distributions

Neglecting to Seek Professional Advice

The complexity of estate taxation often requires expert guidance.

- Attempting to handle complex estates without professional assistance

- Failing to consult specialists for unique situations, such as business ownership or international assets

By being aware of and avoiding these common mistakes, executors and estate planners can ensure more accurate calculations of B.C. taxes on death. This attention to detail can help preserve estate assets, more effectively fulfill the deceased’s wishes, and avoid potential legal and financial complications down the road.

The Impact of International Assets When Calculating Taxes On Death In B.C.

In an increasingly globalized world, many individuals in British Columbia may own assets in other countries. These international holdings can significantly complicate the calculation of B.C. taxes on death, introducing additional considerations and potential tax liabilities.

Understanding Cross-Border Tax Implications

When dealing with international assets, executors must navigate multiple tax jurisdictions:

- Be aware of tax treaties between Canada and other countries

- Understand how foreign tax credits work to avoid double taxation

- Consider the impact of currency fluctuations on asset values

U.S. Assets and Estate Tax

U.S. assets pose unique challenges due to the U.S. estate tax system:

- Canadian residents may be subject to U.S. estate tax on U.S. situs assets

- The current exemption is high, but it’s subject to change

- Strategies like cross-border trusts or life insurance can help manage exposure

Reporting Foreign Assets

Proper reporting of foreign assets is crucial:

- File Form T1135 for foreign property exceeding $100,000 CAD

- Be aware of the Foreign Income Verification Statement requirements

- Understand the penalties for non-compliance, which can be severe

Deemed Disposition of Foreign Property

The deemed disposition rules apply to foreign assets as well:

- Calculate capital gains based on the fair market value in Canadian dollars

- Be aware of any special valuation rules that may apply to foreign assets

Dealing with Foreign Pensions and Retirement Accounts

Foreign pension plans and retirement accounts require special attention:

- Understand how tax treaties treat these accounts

- Be aware of potential withholding taxes on distributions

- Consider the implications of transferring these accounts to beneficiaries

Real Estate in Foreign Countries

Owning property abroad introduces additional complexities:

- Be aware of local inheritance or estate taxes in the country where the property is located

- Understand how foreign property transfers are treated under Canadian tax law

- Consider the impact of foreign currency gains or losses

Offshore Trusts and Corporations

Structures like offshore trusts or corporations require careful handling:

- Understand the tax implications of these entities on the estate

- Be aware of any controlled foreign corporation (CFC) rules that may apply

- Consider the potential for deemed resident trusts

Repatriation of Foreign Assets

Moving foreign assets back to Canada can have tax implications:

- Understand the rules around repatriating funds

- Be aware of any exit taxes that may apply in the foreign jurisdiction

Professional Assistance for International Estates

Given the complexities, professional help is often essential:

- Seek advice from tax professionals with international expertise

- Consider engaging legal counsel in relevant foreign jurisdictions

- Work with financial advisors who understand cross-border estate planning

Staying Compliant with FATCA and CRS

Be aware of international reporting requirements:

- Understand the implications of the Foreign Account Tax Compliance Act (FATCA) for U.S. connections

- Be compliant with Common Reporting Standard (CRS) requirements

Planning for International Assets

Proactive planning can help mitigate tax issues:

- Consider structuring ownership of foreign assets to minimize estate tax exposure

- Explore the use of trusts or holding companies for managing international assets

- Keep detailed records of the original cost and any improvements to foreign property

Dealing with international assets adds a layer of complexity to calculating B.C. taxes on death. Executors and estate planners must diligently understand and address these cross-border tax implications to ensure compliance and minimize potential tax liabilities. Given the intricacies, seeking expert advice is often crucial for estates with significant international holdings.

Future Trends and Potential Changes in Estate Taxation

As we look ahead, it’s important to consider potential changes that may affect B.C. taxes on death in the coming years. While predicting exact changes is challenging, being aware of trends and discussions in the field of estate taxation can help individuals and executors prepare for future scenarios.

Potential Federal Tax Changes when Calculating Taxes On Death In B.C.

Keep an eye on discussions at the federal level:

- Possible adjustments to capital gains inclusion rates

- Potential changes to the principal residence exemption

- Discussions around introducing a federal inheritance tax

Provincial Considerations

B.C. may introduce its changes:

- Potential adjustments to probate fee structures

- Possible introduction of new provincial estate or inheritance taxes

- Changes to property transfer tax rules that may affect estates

International Tax Harmonization

Global efforts to standardize tax reporting may impact estate taxation:

- Increased information sharing between tax authorities

- Potential changes to tax treaties affecting cross-border estates

- Evolving rules around reporting of foreign assets

Digital Assets and Cryptocurrencies

The growing importance of digital assets may lead to new tax rules:

- Clearer guidelines on the valuation and taxation of cryptocurrencies

- Potential new reporting requirements for digital assets

- Evolving rules around the transfer of digital assets upon death

Climate Change and Environmental Considerations

Environmental factors that may influence estate tax policies:

- Potential tax incentives for environmentally friendly estate planning

- Possible new taxes on high-emission assets passed down through estates

Demographic Shifts

Changing population demographics may drive policy changes:

- Potential adjustments to support an aging population

- Possible new rules to address intergenerational wealth transfer

Technological Advancements

Technology may change how estates are managed and taxed:

- Increased use of AI and blockchain in estate administration

- Potential for more sophisticated tax planning tools

- Changes in how digital records are maintained and accessed

Wealth Inequality Concerns

Growing wealth disparity may lead to policy shifts:

- Potential for more progressive estate tax structures

- Possible limitations on tax-free transfers between generations

Small Business Considerations

Changes may be introduced to support family businesses:

- Potential adjustments to the Lifetime Capital Gains Exemption

- Possible new rules to facilitate business succession planning

International Pressure

Global economic factors may influence Canadian estate tax policies:

- Potential responses to changing international tax landscapes

- Possible adjustments to align with global tax transparency initiatives

Simplification Efforts

There may be moves to simplify the estate taxation process:

- Potential streamlining of probate procedures

- Possible consolidation of various tax credits and exemptions

Charitable Giving Incentives

New incentives for charitable bequests may be introduced:

- Potential enhancements to tax credits for charitable donations in wills

- Possible new structures for philanthropic estate planning

Long-Term Care Considerations

The increasing cost of elder care may influence estate tax policies.

- Potential new deductions or credits related to long-term care expenses

- Possible changes to how care-related expenses are treated in estate calculations

While these potential changes are speculative, staying informed about discussions and trends in estate taxation can help individuals and executors prepare for future scenarios. It’s advisable to regularly review estate plans and consult with tax professionals to ensure strategies remain effective in light of any changes to B.C. taxes on death.

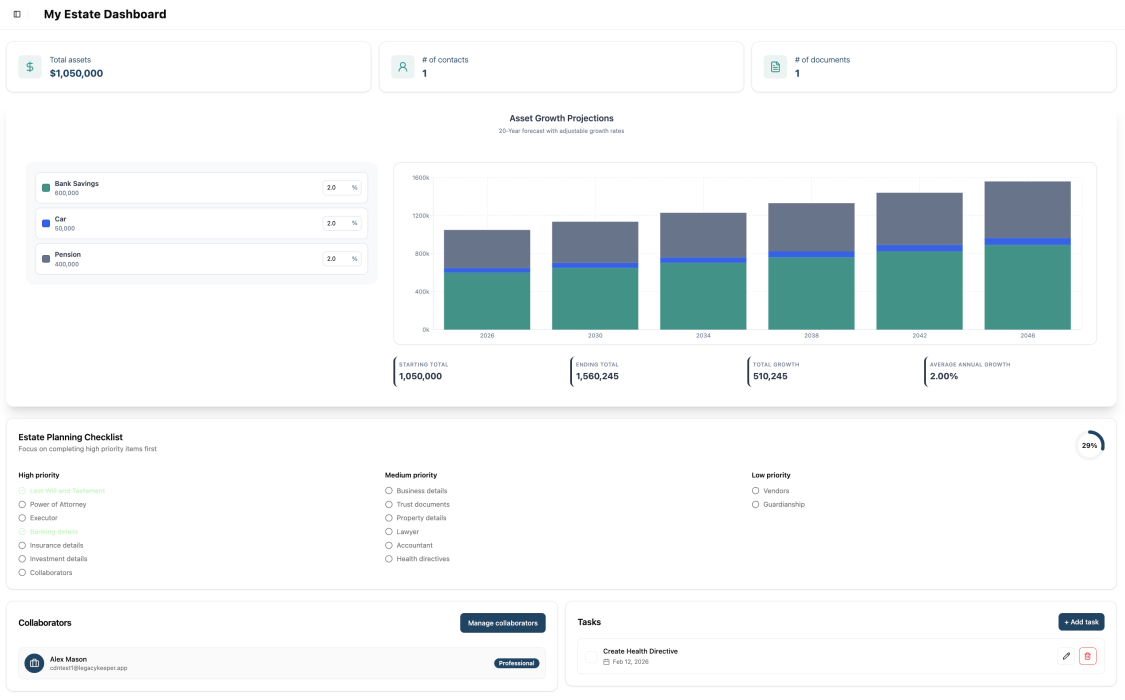

How LegacyKeeper Can Help with Calculating Taxes On Death In B.C.

Having the right tools and support can make a significant difference in the complex landscape of B.C. taxes on death. LegacyKeeper offers a comprehensive solution to help individuals and executors navigate the intricacies of estate planning and tax calculation.

Centralized Asset Management

LegacyKeeper provides a secure platform for organizing and tracking assets:

- Easily input and update information on all types of assets

- Store important documents like property deeds and investment statements

- Track the value of assets over time for accurate tax calculations

Tax Estimation Tools

Utilize built-in calculators to estimate potential estate taxes:

- Input asset values and receive preliminary tax estimates

- Explore different scenarios to understand tax implications

References For Calculating Taxes On Death In B.C.

- https://onyxlaw.ca/inheritance-tax-bc/

- https://my.freshplan.ca/content/MDgyMDI5MQ==

- https://www.nbc.ca/personal/advice/succession/canada-estate-taxes.html

- https://advisors.td.com/daviswealthmanagementteam/mediahandler/media/532685/How%20Much%20Tax%20Do%20I%20Pay%20When%20I%20Die%20_FINAL-April%202023_.pdf

- https://www.cpacanada.ca/news/Canada/2022-04-20-death-taxes-assets

- https://legacykeeper.app/2024/10/07/financial-planning-is-your-roadmap-to-financial-wellness/

Leave a Reply