Attending the 2025 Advise AI conference provided invaluable insights into how wealthtech innovations are reshaping the financial advisory landscape. From agentic AI systems to revolutionary marketing strategies, industry leaders gathered to share perspectives that are fundamentally transforming wealth management. Here are my key takeaways from this event.

What’s New in Wealthtech AI: The Evolution from Chatbots to Agents

One of the most striking revelations at the conference was understanding the fundamental shift occurring in wealthtech AI capabilities. I learned that the industry is moving far beyond simple chatbots to sophisticated agentic systems that can autonomously execute complex, multi-step workflows rather than just answering questions.

These agents function like Lego blocks that can be assembled to automate different processes. The sophistication ranges from no-code solutions that business users can implement themselves to advanced implementations requiring developer expertise. This spectrum means that firms of all sizes and technical capabilities can participate in the agentic AI revolution.

Another major shift I observed was in how information discovery is changing. Traditional search engine optimization is giving way to what presenters call answer engine optimization (AEO). Instead of providing lists of links, AI tools now provide direct answers. This fundamentally changes the game for financial advisors trying to be discovered by potential clients.

Top Use Cases for AI in Wealth Management

Throughout the conference, I saw numerous practical applications of wealthtech AI that firms are already implementing with measurable results.

Account Opening and Administrative Automation

What impressed me was seeing how AI agents can now access household information and CRM data to populate applications while the advisor remains on the phone with the client. This transformation of a 20-30 minute process into a real-time conversation fundamentally improves the client experience while dramatically increasing efficiency.

Meeting Intelligence and Preparation

The most widely adopted wealthtech tool I heard about was meeting note-takers, which have evolved far beyond simple transcription. One presenter shared an insight that resonated with me—client service staff can now access meeting chat logs to find answers to specific questions without interrupting advisors.

For example, when staff need to know which IRA a distribution should come from, they can search the meeting notes rather than sending an email and waiting for a response. This seemingly slight improvement eliminates frustration and dramatically speeds up operational workflows.

Multiple speakers highlighted the human element that I found particularly compelling. Advisors report that with AI handling notes, they can put their pen down, maintain eye contact, and deliver a more personal client experience. This is AI enhancing human connection rather than replacing it.

Compliance Monitoring and Risk Management

I learned that compliance agents will become increasingly critical as communication volumes grow. AI can monitor communications at scale, flagging potential issues for human review rather than creating bottlenecks by manually overseeing every interaction.

Client Intelligence and Next Best Action

Several firms are developing tools that surface opportunities for advisors to grow their business and better monitor portfolios. The challenge of keeping track of 100+ clients and identifying timely opportunities is precisely where AI can provide the most value. I was impressed by the vision of AI systems that proactively alert advisors to client life events, portfolio rebalancing needs, or service gaps.

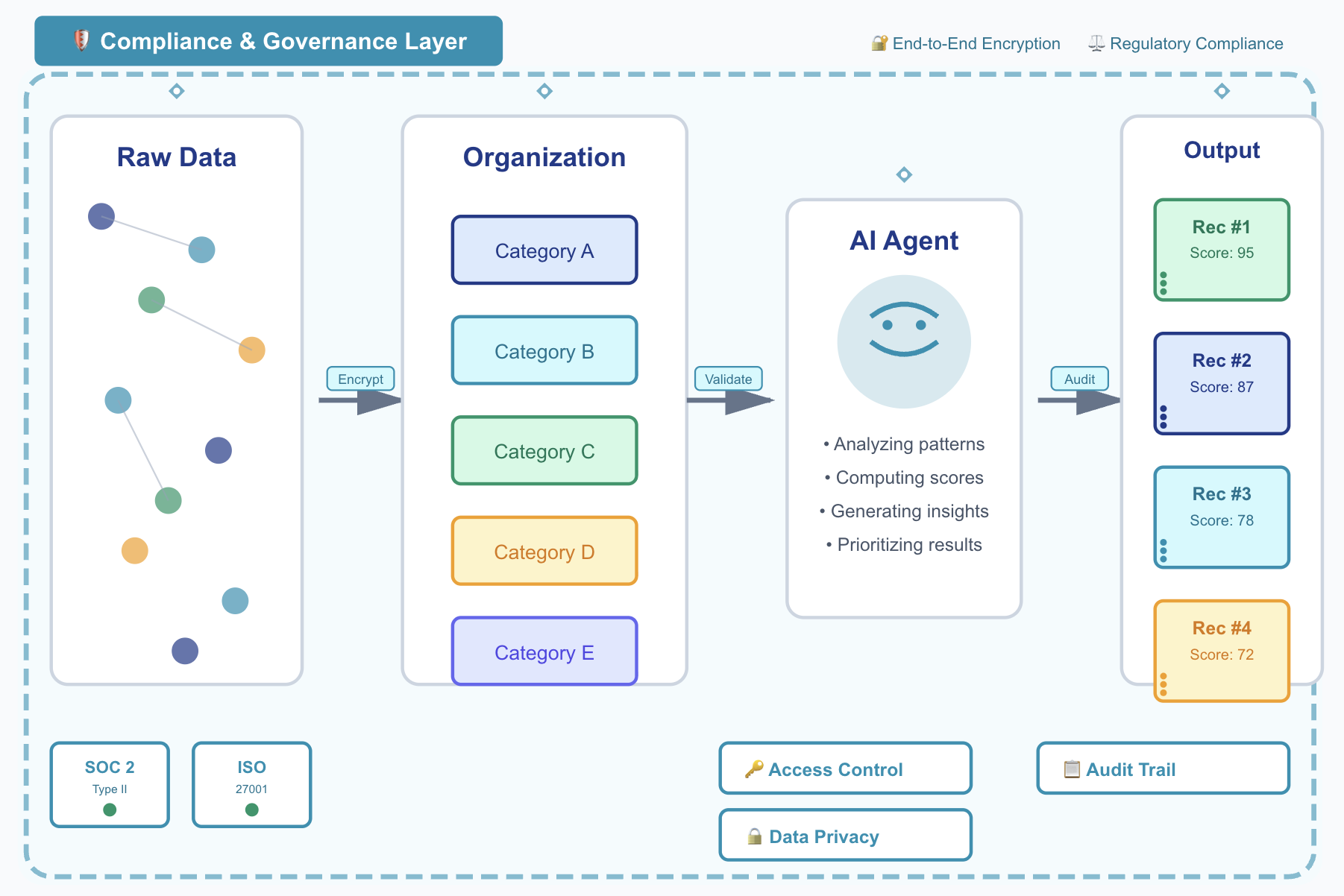

The Critical Role of Data Organization in Wealthtech AI Success

The most important theme I took away from the conference was that clean, well-organized data is the absolute foundation for AI success. No amount of sophisticated AI can overcome poor data quality and organization.

The Data Challenge Facing Advisory Firms

One presenter painted a picture that many advisors will recognize. Firms are juggling multiple systems, data gets siloed, and pulling everything together becomes incredibly difficult. What really struck me was the description of the common scenario where firms insist they have no data issues. Still, when you dig in, you find rep codes set to “zero zero zero,” mysterious accounts, and critical knowledge held by just one or two people. This creates a vulnerability that isn’t scalable for growing businesses.

The Integrated Data Ecosystem Approach

I learned about the concept of an integrated data ecosystem, which was supported by a recent Gartner study on the future of technology architecture. The traditional model of on-premise servers evolving to cloud-based SaaS applications is now giving way to something new.

The future involves creating a centralized data foundation—a data platform—where apps and AI agents share a common data source. This represents a fundamental architectural shift in how advisory firms should think about their technology stack.

The Data Lakehouse Concept

One of the most innovative solutions I encountered was the data lakehouse concept explicitly built for wealth management. This involves centralized storage, where all applications and data reside in one place, connected through a common platform with an open architecture that allows any vendor to build integrations. What validated this approach for me was learning that this concept was recently recognized by Gartner as the recommended approach for financial services, specifically because it addresses the unique needs of wealth management, such as entitlement structures and rep codes that are distinct to our industry.

Why Data Centralization Matters for Wealthtech AI

The typical advisory firm technology stack creates significant friction for AI implementation. I heard descriptions of firms where accounting systems sit disconnected from client-facing tools, requiring staff to access multiple systems to complete simple workflows. With a centralized data lakehouse approach, all data resides in a single location, eliminating the need to move it between systems. This means applications become agents that execute workflows or leverage that data to provide capabilities, analytics, and streamlined onboarding. One smaller advisory firm shared its practical experience that resonated with me. Even with this more integrated approach, there’s still some implementation effort, but it’s about a quarter of what it was before in terms of timeline and complexity. Most importantly, firms can focus on finding the right people rather than the right technology compatibility.

The Four-Step Process for Data Preparation

I found the systematic approach to data organization particularly actionable:

- Organize your data: Get to the point where you have clean, reliable data. This means checking for issues such as incorrect rep codes and accounts with placeholder identifiers, and understanding where tax information is stored across different systems.

- Evolution step: Add capabilities and bring applications into your data ecosystem, building on that solid foundation.

- Innovation: Once you have organized data, it becomes much easier to build with AI technologies. What used to require extensive development resources 10 years ago is now accessible with AI agents, with the programming process accelerated by at least 10-fold.

- Deployment: Deploy AI applications directly on top of your data foundation.

AI-Ready Data Requirements

Firms need to prepare to act on AI opportunities early, and the most crucial thing any firm can do is organize its data well and keep it clean.

This preparation involves:

- Consistent formatting: Ensuring data is structured consistently across all systems

- Complete records: Having comprehensive information that AI can access

- Accessible integration: Making sure data can be easily pulled into AI workflows

- Ongoing maintenance: Continuously updating and cleaning data as part of regular operations

The Competitive Advantage of Clean Data

I came away understanding that data preparation isn’t just about enabling AI—it’s about competitive advantage. Firms investing in their data foundation now will be much better positioned when more sophisticated AI capabilities emerge. The payoff is significant. Vendors are moving from complex, multi-month integration projects to simple drag-and-drop deployments, with AI applications running on clean data with no integration required.

Top AI Marketing Strategies for Financial Advisors

There are three critical approaches for financial advisors to succeed in the AI-powered search landscape, representing a significant shift in wealthtech marketing.

1. Getting Reviews and Building Social Proof

I learned about the fundamental shift in how reviews function in the AI era. Reviews are social proof that sends a sentiment signal to AI. The job of modern AI search tools is to give the best, most obvious answer to whatever someone is asking, and one way they determine this is by asking whether real human beings have used a particular business.

The absence of reviews now creates suspicion from the consumer’s perspective. A few years ago, when no financial advisors had reviews, it was normal. Now that some advisors have them, firms without reviews look strange to potential clients.

The content of reviews matters significantly for wealthtech AI discovery. The language used in reviews gets tied to your brand, and the more you’re mentioned along with specific phrases, the more you’ll be known for those services. When someone mentions specific services or expertise in a review, AI tools recognize those associations and are more likely to recommend that advisor for relevant queries.

2. Building Authority Through Earned Media

Wealthtech AI systems show a strong preference for advisors featured in credible publications. Key sources that AI tools trust include industry publications, online forums, and press releases. Press releases are particularly effective in 2025 because they are published on multiple sites and indexed by AI systems.

One fascinating insight was that specific online forums have become the most cited domains in AI overviews. AI tools are looking at these forums because real people visit them to search for information or discuss brands and services. Even if you don’t actively contribute, these forums provide insights into the types of questions people are asking, which can inform content creation using the actual language of your target audience.

3. Formatting Content for AI Discoverability

The shift from SEO to AEO requires fundamental changes in content strategy. Before, it was about ranking for keywords. Now it’s about giving straightforward answers. We used to want to rank for simple location-based keywords, but now we need to be much more specific based on how people ask AI tools questions.

Modern searches include extensive context. People might describe their age, profession, business ownership status, location, family situation, and specific needs in a single query. This means advisors need to create content that addresses these particular scenarios.

The key insight I took away was to structure content as questions and answers—the more you can format it as actual questions people would ask, the better your chances are of being picked up by AI.

I also learned about schema markup, which is backend website code that helps AI tools find specific information, such as location data and contact information, more easily. This technical optimization is becoming essential for AI discoverability.

How to Best Leverage AI in Your Practice

Industry leaders at the conference emphasized strategic implementation over rushing to adopt every new wealthtech tool.

Implement a Risk-Based Framework

I learned about a practical framework for categorizing AI use cases into three risk levels:

- Low risk: Productivity tools like AI note-takers, which are becoming table stakes for modern practices

- Medium risk: Decision support with human intervention, which presenters described as the most exciting opportunity

- High risk: Systems that make autonomous decisions, particularly in investment advice

The key insight was that firms should focus primarily on low and medium-risk applications with proper human oversight. For any applications you’re concerned about, the recommendation was to update disclosures to indicate you’re using AI. Since the regulatory regime for investment advisors is based on disclosure and transparency, this same principle should apply to AI usage.

Focus on Human Intervention Points

When you break down something like meeting preparation, it’s aggregating data, so you can put extensive automation into that process.

However, clear boundaries are essential. Anything that creates, updates, or changes information about the client should never be fully automatic. Emails shouldn’t go out automatically, and client communications must be reviewed by the advisor before being sent.

Start with Client-Facing vs. Internal Tools

One practical decision framework was distinguishing between client-facing and internal tools. Firms should be much more cautious with client-facing tools. With internal operational tools, there’s more flexibility to try things and unplug them if they don’t work. But advisors don’t want to constantly be plugging and unplugging tools clients interact with.

The advice was to find products and teams building for the future, not just offering a solution for right now. Looking at a vendor’s roadmap and vision for evolution is critical.

Invest in Training and Education

A critical gap identified at the conference was that while many advisors are using AI today, few feel they use it well. One major firm reported hosting peer-sharing sessions at their conferences where advisors teach other advisors, and these sessions were filling thousand-person ballrooms.

The emphasis was that effective AI use requires investment. It takes at least 10 hours of playing with these tools to learn how to use them effectively. Modern AI tools have been trained on the knowledge of advanced financial professionals, but users need to learn how to leverage that training effectively.

Top Wealthtech AI Concerns and How to Address Them

Despite enthusiasm for wealthtech innovations, compliance and security concerns remain paramount.

Privacy and Data Security

If you’re registered with the SEC or state regulators, there are rules governing how you must safeguard client non-public information.

Firms need reasonably designed policies that can safeguard information, including appropriate access controls to prevent unauthorized access, encryption, proper employee training, and the ability to respond to security breaches.

The emphasis on due diligence was strong. Whether evaluating a regulatory technology provider, sub-advisor, or AI vendor, firms need to show initial and ongoing due diligence. This includes checking for security compliance certifications and understanding how data will be used during the due diligence process.

Accuracy and Hallucinations

The challenge of AI hallucinations was acknowledged as making people scared to use these tools. Firms can ensure inputs are well-defined and provide context, use proper prompting and training, tell the tools to show their work, and use human intervention to review outputs.

One firm described its rigorous approach called red teaming. Before even thinking about integrating a use case, it goes through a vigorous process where internal and external teams try to break it, understanding the level of hallucinations and the propensity for it to distribute personally identifiable information.

Bias and Fiduciary Duty

Bias occurs when using general AI platforms because they’re trained on information that’s already been fed into the system. This creates fiduciary concerns because advisors owe duties to their clients, including the duty to provide advice in clients’ best interests and the duty of loyalty to ensure advice isn’t conflicted.

Books and Records Compliance

A critical compliance challenge was highlighted around record retention. Regulatory rules require advisors to keep extensive records, but the challenge is determining which inputs and outputs must be retained as official books and records. Many advisors use personal accounts with consumer AI platforms, which creates retention problems at the firm level. Enterprise solutions that enable proper record retention are becoming an essential part of wealthtech infrastructure.

Establishing AI Governance

The recommendation I heard was to implement formal oversight through either an AI officer or a committee. The key message was that if you’re worried about hindsight—potential mistakes or changes in regulatory sentiment—having documented governance is critical.

The emphasis was on documentation. If you make a good-faith effort to use AI with professional due diligence processes, similar to how you would document investment committee decisions, the specific governance structure matters less than the documentation itself.

The Future of AI Agents in Financial Planning

The wealthtech industry is entering what experts call the “agentic era,” where AI systems move from assisting to autonomously executing complex workflows.

From Copilots to Autonomous Agents

We’re now in an era where we’ve pivoted from copilot assistance to autonomous agents. What these agents can actually automate depends entirely on the tools they plug into. Concrete examples included combining optical character recognition tools with ticket creation systems to analyze a client’s statement, identify complaints, and automatically create a ticket for back-office teams.

The Importance of Orchestration

Firms must maintain control over their AI architecture through orchestration. The approach described was to build systems like Lego blocks—integrating best-in-class tools while developing internal differentiators. The key differentiator is owning the AI orchestration layer. Even when using specialized tools for financial or tax planning, the firm’s system should determine where you go and how you get there, rather than having the AI decide what’s next. This ensures proper governance and control.

Modular Architecture and Integration

The future of wealthtech development will be modular. Historically, firms exposed functionality through APIs. The next level involves new protocols and micro front-ends so that each app has its own minimal user experience that can be dropped into chat interfaces or agentic workflows.

A critical point emphasized was transparency. Understanding what the AI language model is doing versus what a traditional application is doing will be really important for agentic AI systems. Users need to know when they’re interacting with AI versus when specialized business logic from trusted applications is being used.

Beyond Simple Automation: Life Event Support

One vision that excited me was thinking bigger about agent capabilities beyond basic transactions. Using the example of having a child, the presenters challenged the notion that opening an education savings account is what new parents focus on—it’s nowhere near the top of their list of priorities.

The vision was for agents that could help with multiple aspects of life events: evaluating how well current health coverage meets a growing family’s needs, analyzing childcare options and their tax implications, and generally helping clients research and make decisions around major life transitions. AI can dramatically accelerate the research process for these complex decisions.

The Consolidation Question

The consensus is that we’re already seeing people ask how these tools integrate and work together. Everyone recognizes there are over 600 companies on the fintech map right now, and firms don’t want to have six different AI applications. If the industry can bring solutions together, that would be much more powerful. While there’s discussion of business logic moving from the traditional software layer to the AI layer, specific applications, like financial planning, require business logic that must remain deeply understood and well thought through.

The predicted future is a hybrid model that separates business logic from user experience. We’ll see business logic separated from the user interface layer, and users might not realize when working in an aggregated interface that traditional applications are actually running behind the scenes.

Conclusion: Embracing Wealthtech’s Transformative Moment

The 2025 Advise AI conference made clear that wealthtech is at an inflection point. The transition from basic chatbots to sophisticated agentic AI systems represents not just an incremental improvement but a fundamental restructuring of how financial advisory practices operate.

The most successful firms are taking a measured, strategic approach to wealthtech AI adoption—starting with data organization, implementing robust governance frameworks, and gradually moving toward more complex use cases as they build confidence and expertise.

One insight that resonated deeply with me was that AI is not just a tool; it’s a business model. There are so many complexities and interdependencies around a change like that, and it just doesn’t all come together overnight.

The wealthtech revolution isn’t about replacing human advisors—it’s about amplifying their capabilities to deliver deeper, more personalized client service.

For financial advisors, the message is clear: wealthtech AI adoption is no longer optional. Those who thoughtfully integrate these tools—starting with clean, organized data as their foundation—are already seeing measurable advantages in efficiency, client satisfaction, and business growth. The future belongs to advisors who can successfully blend cutting-edge wealthtech with the irreplaceable human elements of empathy, wisdom, and trusted guidance.

FAQ

Q: What is the difference between chatbots and agentic AI in wealthtech?

A: From what I learned at the conference, chatbots primarily handle Q&A interactions, while agentic AI systems can autonomously execute complex, multi-step workflows. Agentic systems are moving us toward a world where they execute workflows rather than respond to queries. Agents can be assembled like Lego blocks to automate different processes.

Q: Why is data organization so critical for AI implementation?

A: This was the most important takeaway from the conference. Poor data organization is the most significant barrier to successful AI adoption. Data is often siloed across multiple systems, with knowledge residing in just one or two people’s heads, which isn’t scalable for growing businesses. AI requires clean, centralized data to function effectively. Firms need to reach a point where they have clean, reliable data before implementing AI solutions.

Q: What is a data lakehouse, and why does it matter for wealthtech?

A: A data lakehouse is a centralized storage platform where all applications and data sit in one place. It provides a common platform with open architecture so multiple vendors can build integrations. This approach was recently recognized by industry analysts as the recommended approach for financial services because it addresses wealth management’s unique needs, such as entitlement structures and rep codes. This architecture allows AI agents to access all necessary data without moving it between systems.

Q: What are the most common AI use cases in wealth management today?

A: The top wealthtech AI applications I saw presented include meeting note-taking and transcription, account opening automation, meeting preparation and client intelligence, compliance monitoring, content creation, and CRM data synthesis. Meeting note-takers remain the most widely adopted tool, with multiple firms noting that client service teams find them game-changing for efficiency.

Q: How can financial advisors improve their visibility in AI search results?

A: I learned three key strategies: (1) obtaining client reviews that include relevant keywords and context, (2) building authority through earned media in industry publications and online forums, and (3) formatting content for AI discoverability using conversational language, Q&A structure, and schema markup on your website.

Q: What are the main compliance concerns with AI in wealth management?

A: Four primary concerns were outlined: privacy and data security (regulatory compliance with data protection rules), accuracy of data, preventing hallucinations, avoiding bias in AI recommendations, and maintaining proper books and records retention of AI interactions. Many advisors using personal consumer AI accounts create compliance problems with record retention at the firm level.

Q: Should firms use free AI tools or invest in enterprise solutions?

A: For most compliance and data security purposes, enterprise solutions are strongly recommended. Personal consumer AI accounts create retention problems at the firm level. Enterprise solutions provide better control, security, audit trails, and compliance capabilities, which are essential for regulated firms.

Q: How should firms categorize AI use cases by risk level?

A: The framework I learned includes three categories: (1) Low risk—productivity tools like note-takers, (2) Medium risk—decision support with human intervention, described as the most exciting opportunity, and (3) High risk—systems making autonomous decisions, particularly in investment advice. Most firms should focus on low and medium-risk applications with proper human oversight.

Q: Will AI enable advisors to serve larger books of business?

A: The industry appears divided on this question. Some predict that advisors will manage 250-300 clients, up from today’s average of 150, while others suggest that AI will enable deeper service to smaller, more focused client bases.

Q: What steps should firms take to prepare their data for AI?

A: I learned a four-step process: (1) Organize your data—ensure it’s clean and reliable, fix issues like incorrect rep codes and account identifiers, (2) Evolution—add capabilities and bring applications into your data ecosystem, (3) Innovation—build new AI-powered solutions on your data foundation, and (4) Deployment—launch AI applications that work directly with your centralized data.

Q: How necessary is ongoing training for AI adoption?

A: Training is critical. While many advisors are using AI today, few use it well. It takes at least 10 hours of playing with these tools to figure out how to use them effectively, because they contain extensive knowledge from advanced financial professionals that users need to learn to access properly.

Leave a Reply